Unless you’ve been living your best, unbothered life on a remote island in Bali, then you know, the Supreme Court made the decision to block the Biden administration’s student debt relief plan. This plan would have permitted the discharge of up to $20,000 of federal student loans for approved applicants. The ruling, which was issued on June 30th, may have disrupted the plans of what the White House estimated to be $26 Million people2 who applied or were eligible for one-time debt relief. If you are one of those borrowers, here’s what you need to know about the new SAVE Repayment Plan and other Repayment Options to help you finally get rid of your student loans.

The SAVE Repayment Plan

The Saving on a Valuable Education (SAVE) Repayment Plan, released immediately following the Supreme Court’s ruling, will provide some borrowers with leeway in repaying their federal student loans. The plan will replace the existing REPAYE plan and those that are already enrolled in the REPAYE plan will be automatically grandfathered into the new SAVE repayment plan.

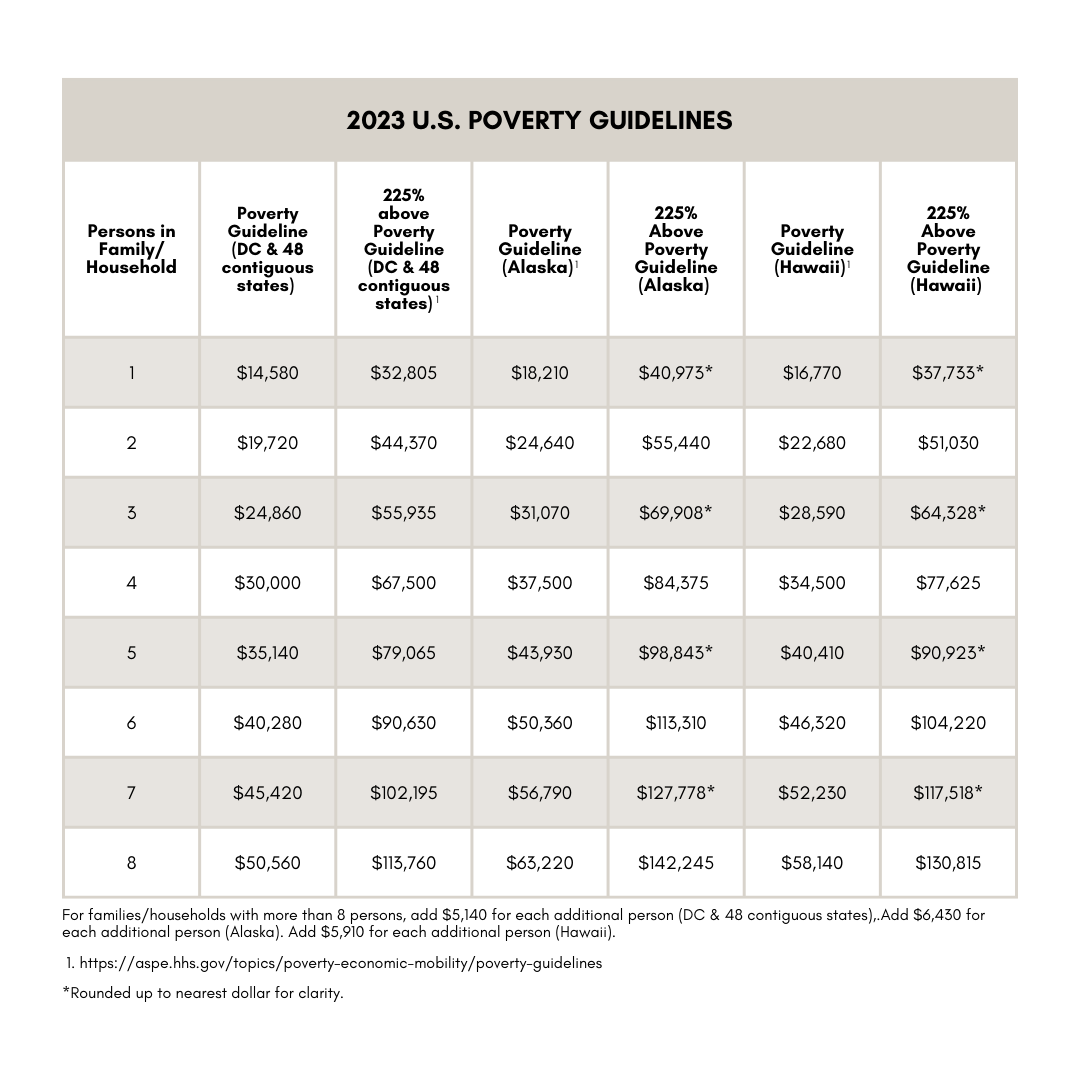

The SAVE Repayment Plan, reduces the discretionary income utilized to calculate your payment to within 225% of the poverty guidelines as shown in the table below.

With the SAVE Repayment plan, interest does not accumulate. Per StudentAid.gov, “The plan eliminates 100% of remaining interest for both subsidized and unsubsidized loans after a scheduled payment is made under the SAVE Plan.” That means, if $30 in interest has accumulated and you make your required minimum payment of $25, $5 of interest will be discharged.

Lastly, if you are married and file your taxes separately, your spouse’s income will not be included and therefore, you will not need your spouse as a cosigner on your income driven repayment application.

There are additional benefits that are planned to go into effect in 2024, the most significant being a reduction of minimum payments from 10% of income above 225% of the poverty line to 5%. You can find the rest on Student Aid’s website.

If you want to consider some alternatives to the SAVE Repayment Plan, and are seeking public service loan forgiveness, here are some options:

- Pay As You Earn (PAYE) Repayment Plan – The PAYE Repayment plan, not to be confused with the REPAYE plan which is going away, is an option available for those with Direct Subsidized and Unsubsidized loans, Direct Plus loans made to students, or Direct consolidation loans (Parent PLUS loans not included). The PAYE Repayment plan will provide a payment that is less than the standard payment and your payment amount is adjusted on an annual basis based on your income and family size. You can expect your payment to be around 10% of your discretionary income. With this plan, you’ll typically pay more overall than if you utilize the Standard Repayment Plan. However, if your cash flow is tight, this option may provide you with some flexibility.

- Income Based Repayment (IBR) Plan – Under the Income Based Repayment Plan, your minimum required payment will be between approximately 10% to 15% of your discretionary income. If you are married filing jointly, your spouse’s student loans and income will be considered in determination of your payment amount. Your payment may be modified on an annual basis as you update your income and family size each year.

- Income Contingent Repayment (ICR) Plan – Like the PAYE Plan, you must have either a Direct Subsidized and Unsubsidized loan, Direct Plus loan made to students, or Direct consolidation loan (Parent PLUS loans not included) to be eligible for this plan. The amount of your payment will be the lesser of either 20% of your discretionary income or the amount you would need to pay to have your loan paid off in 12 years, with an adjustment based on your income. Yes, I know that is confusing. Like the other income-based repayment plans, you will need to update your income and family size on an annual basis to determine what your payment will be each year. If you are married filing jointly or signed up to pay your Direct loans jointly with your spouse, your spouse’s student loans and income will be considered in determination of your payment amount.

Additionally, Public Service Loan Forgiveness (PSLF) is a viable option for many of our clients and integrates with the aforementioned repayment plans. PSLF was designed to provide student loan forgiveness for those who work in public service sectors for governmental or not-for-profit organizations. After making 120 payments while working for a qualified employer, the remainder of your loan balance is forgiven. This is especially beneficial for those who have large loan balances.

Not all student loan repayment plans qualify under the rules of the Public Service Loan Forgiveness (PSLF) program, so it is important that you verify PSLF eligibility before selecting a repayment plan option. However, the options listed in this blog are PSLF-friendly. To get a better idea of which option would best suit you, try Federal Student Aid’s Loan Simulator.

At this point, you probably just want to know what to do, so here are some steps you can start taking today.

- Check your loan balance and determine if it is large enough to warrant making changes to your payment plans. If your balance is relatively low, begin making payments once the forbearance period is over.

- If you are a nurse or other public service professional who has not applied for PSLF, use the PSLF Employer Search tool to determine if you work for a qualified employer.

- If your employer is qualified, complete the PSLF application.

- If you want to apply for PSLF, but your Federal Family Education Loan (FFEL) loans aren’t currently held with the federal government, consider a one-time consolidation with the federal government. In doing so, from now until the end of 2023, you will be eligible for a one-time look back to count all payments you have made while working for a qualified employer.3

- Use the Loan Simulator tool to find a repayment plan that works best for you.

- Start planning your budget for when the forbearance period is lifted.

- If you are enrolled in the PSLF program, set a reminder to submit your employment certification form on a periodic basis to qualify your eligible student loan payments throughout the year.

If you want a personal strategy to not only pay off your student loan, but to achieve your other quality-of-life goals, schedule a free consultation to see how we can serve you.

- Poverty Guidelines | ASPE (hhs.gov)

- FACT SHEET: Biden-Harris Administration Releases New Data Showing 26 Million People in All 50 States Applied or Were Automatically Eligible for One-Time Student Debt Relief | The White House

- Payment Count Adjustments Toward Income-Driven Repayment and Public Service Loan Forgiveness Programs | Federal Student Aid