By Daniel Dorval, CFP®

The recent failure of Silicon Valley Bank along with a couple other at-risk financial institutions has been well publicized in our crisis-du-jour media. We also learned Credit Suisse was bought out by UBS through a Swiss government facilitated sale. These tremors in the banking system have rightfully caused some concerns about the safety of cash reserves and potential impacts on markets.

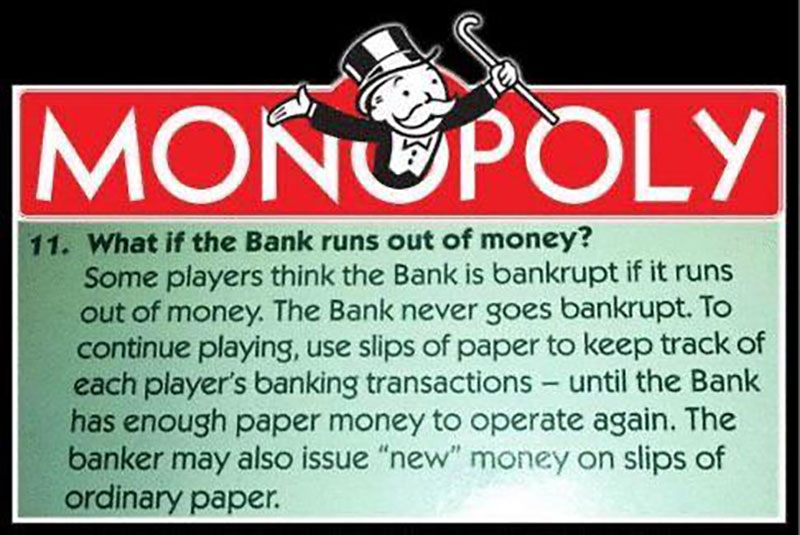

We think it is the beginning of unwinding some of the Federal Reserve-induced speculative bubble from keeping interest rates very low for a long time. Rates have risen considerably and we are likely to continue seeing speculative risk get punished while prudent saving and investing gets rewarded long term. The Federal Reserve basically went from full on the gas (contributing to inflation) to hard on the brakes (to reduce inflation). There is an old saying that when the Fed hits the brakes, someone might go through the windshield…that is what we experienced over the past couple weeks with banks that did not properly address their interest rate risks. I wanted to share that we have all been through this before. It was when we were kids and played Monopoly! This is part of the official Monopoly rules that I pulled from our game:

“The Bank never “goes broke.” If the Bank runs out of money, the Banker may issue as much more as may be needed by writing on any ordinary paper.”

“Ordinary paper” has now been replaced by electronic funds transfers from Washington, DC! The Monopoly banker is the Federal Reserve. US banking authorities created a new financial backstop for banks to help protect cash deposits. It is called the Bank Term Funding Program and the Federal Reserve considers it big enough to protect ALL deposits. They have plenty of Monopoly money!

At this point we do not believe there will be any issues at any of the major local, regional, or national banks. The failures in California and in Europe are significant, but those institutions had unusual circumstances that should not apply to most of the retail banks we and our clients are using. It is also an important reminder that most major financial institutions have insurance to help protect consumers in the case of a failure. This is probably not a good time to exceed FDIC insurance limits on cash reserves. Deposit insurance is how the FDIC protects your money in the unlikely event of a bank failure. The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. They have a calculator on their website if you have concerns about exceeding the insurance amounts: FDIC: Electronic Deposit Insurance Estimator (EDIE).

Brokerage firms like TD Ameritrade are SIPC insured. It is extremely rare to have a brokerage firm fail, but in the unlikely event, SIPC helps cover fraudulent loss of cash and securities. I thought it was interesting to see that the only open case before SIPC is the Bernie Madoff fraud case from 2008! We have no concerns about any of the custodians we use to hold our client investment accounts. We wanted to share our thoughts and reassure everyone the banking system has significant resources to keep it safe and functioning normally for regular people like us. There is no reason to take actions other than maybe verifying any bank cash reserves are within FDIC insurance limits just to be cautious.To learn more about Quality of Life Planning®, click here. If you need help aligning your money with your values, priorities, motivations, and goals, schedule a meeting with us. It would be our pleasure to assist you.